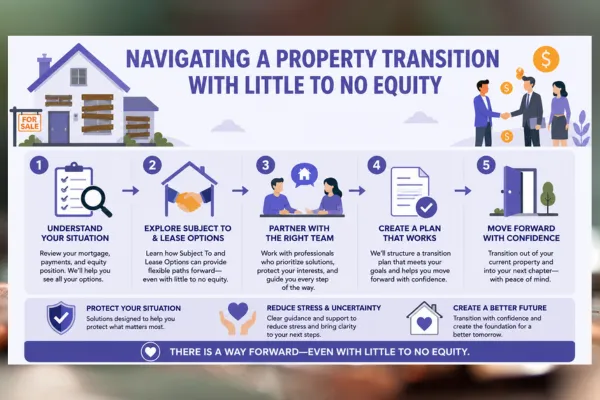

Navigating a Property Transition With Little to No Equity

Understanding the Low-Equity Dilemma

When most people think about selling a home, they assume there will be a substantial cash profit left over at the end of the transaction. However, if you purchased your property recently with a low down payment, or if local market conditions have shifted, you might find yourself owning a house with little or no equity.

In a traditional retail sale, a lack of equity creates an immediate financial roadblock. Between standard real estate agent commissions, county transfer taxes, escrow fees, and title insurance charges, selling a home conventionally costs roughly 8% to 10% of the total purchase price. If your property does not have enough equity to cover these transaction costs, you are legally required to bring your own out-of-pocket cash to your closing table just to hand over the deed.

For many homeowners, paying thousands of dollars out of pocket to sell a house is simply not a realistic option. Exploring alternative, non-traditional real estate setups allows you to look at practical structures designed to bypass these retail transaction costs completely.

How Alternative Structures Provide Relief

When you move outside the traditional retail market, a property's value matters less than the underlying structure of the debt. Alternative transactions use private, direct contracts that don't rely on standard retail agents or conventional bank refinancing. This allows high-leverage homeowners to unlock direct benefits:

🔹 Eliminates Real Estate Commissions: Because the transaction is negotiated directly between the participants out of escrow, standard 5% to 6% agent fees are completely removed from the equation.

🔹 Bypasses Out-of-Pocket Closing Costs: Creative frameworks are structured so that the incoming buyer covers the closing expenses, allowing the seller to transition out of the property without writing a check at closing.

🔹 Protects Your Credit Profile: If a sudden change in billing status or a relocation timeline makes it difficult to maintain ongoing housing costs, alternative arrangements resolve the debt safely before any formal delinquency notices are recorded.

Practical Frameworks for Low-Equity Houses

Depending on your mortgage balance and your immediate moving goals, there are two primary structures commonly explored for low-equity property transitions:

1. Subject-To Arrangements

In a Subject-To setup, a buyer purchases your home subject to the existing financing. The legal title and deed transfer to the buyer, but your original mortgage stays in place. The buyer agrees to take over full financial responsibility for making your ongoing monthly payments, taxes, and insurance directly. This allows you to walk away from the property debt cleanly, without needing equity to pay off the loan balance upfront.

2. Structured Lease-Options

A Lease-Option serves as a flexible bridge solution. A buyer signs a formal lease agreement to occupy and maintain the home, while securing a contractual right to buy the asset at a later date once more equity has naturally built up. The incoming party handles the day-to-day property logistics and rental income, covering your monthly mortgage statements while you move forward with your relocation plans.

The Bottom Line

Owning a property with little or no equity does not mean you are trapped or forced to pay out-of-pocket fees to move. It simply means the traditional retail market is the wrong tool for your situation. Learning how alternative note and financing structures handle property debt ensures you can evaluate your choices calmly, protect your financial security, and exit on your own terms.

Want to see which alternative framework fits your specific situation? Check your details using our interactive tool.